How Venture Capital Decision Making Has Changed During the Pandemic

The sudden arrival of the global pandemic has shifted the playbook for founders and venture capitalists. Despite the beginnings of a vaccine rollout, it’s likely that the conditions created by Covid-19 will continue to persist for some time. Zoom calls have taken the place of in-person meetings. Investors previously prone to onsite visits and amassed airline miles, now grapple with how to form relationships and build confidence without having met teams in person. At NextView, we’ve experienced this changing environment first hand. As high-conviction, seed stage investors, we are inherently relationship-driven, and we value meeting exceptional founders face-to-face.

With the onset of COVID-19, we, along with the broader ecosystem of venture capitalists and entrepreneurs, have been pushed to rapidly adapt, forge connections, and do our jobs remotely. Noting our own experience, we questioned whether the fast proliferation of virtual interaction introduced by the COVID-19 crisis had changed investor decision-making more broadly across the venture capital industry. We interviewed various VCs about COVID-19 thinking and decision-making, and potential implications for the fundraising process.

Here’s what we’ve seen from our own activity, the activity of our coinvestors, and multiple interviews conducted with GPs at both seed, series A, and multi-stage funds.

How has this period impacted your pace of investment?

Following initial decision paralysis, many venture capitalists have returned to pace

There was a meaningful drop in venture capital investments in the early months of the pandemic, as the U.S economy shut down and investors grappled with new waves of uncertainty. In a survey conducted by Stanford’s Strebulaev and co-researchers, over 1,000 institutional and corporate venture capitals reported that investment pace was 71% of normal in the first quarter of the pandemic, with roughly ¼ adding that they had struggled to evaluate new deals. The majority had dedicated more time to guiding the portfolio companies through the pandemic.

Kent Bennett from Bessemer Venture Partners spoke to this initial slow down: “We couldn’t do anything until we understood the new normal. Many of the investments I was pursuing in this period were smaller checks, with the intent to invest more when the world came back to life.”

However, the sector has been fast to adapt, as entrepreneurship persists and leads to new forms of recovery. Gradually adjusting to sourcing deals online, venture capitalists invested $37.8 billion across 2,288 deals in Q3, with deal count exceeding Q2’s at nearly every stage.

Early stage deal activity showed real resilience coming off of a slow Q2, with deal count at angel and seed stage in 2020 now about at par with the same period in 2019. Despite the sustained climate of uncertainty, valuations continued to climb and VC exit values reached their second highest total ever in Q3.

VC fundraising has also remained strong as firms look ahead, with VCs raising $42.7 billion in 148 funds for the first half of 2020. Over the last decade, only three years saw higher VC fundraising numbers than that seen in the first six months of 2020.

Graham Brown from Lerer Hippeau commented on this rapid recovery: “We saw a large slowdown in March, April, and May, before our speed really picked up in June. Much like investors, a lot of entrepreneurs that didn’t need fundraising stopped seeking investment until they had a better sense of what was happening in the world. This opened up a significant backlog, leading to the most active summer period we’ve ever seen.”

Lily Lyman from Underscore VC echoed this momentum: “Q2 and Q3 have been some of our busiest quarters from an investment perspective.”

By cutting out logistics, the top of the deal funnel has gotten wider and more efficient

There is less wasted time in ubers, repeated cross-country trips to board meetings and conferences. This leaves more space for more top of funnel activity: for back-to-back Zoom calls that create and expand relationships with new and known founders.

For some, this shift is a long time coming. Said one investor, “We may have overdone it on socialization at the expense of productivity.”

Of the eight venture capitalists we interviewed, six commented that they felt more efficient and were able to have more early conversations during this period than before. This included investors at Bain Capital Ventures, Upfront Ventures, and Bloomberg Beta.

One firm added that gained efficiencies have meaningfully expanded the top of their deal funnel: “ Our investment team has been able to have 2X the amount of top of funnel meetings than they’d have previously. By cutting out the commute, the process becomes much more efficient. You can realize fast if there’s not a fit, to avoid wasting both your and the entrepreneurs time. You can meet more teams and hear more ideas.”

Greg Bettinelli at Upfront Ventures added “There is less parking time, less in between time, and more time in the day. I can have a wider reach and a higher volume of 30 minute meetings with founders.”

While it was easy to conceive that virtual modalities would widen top of the funnel conversations, our questions remained about how this period would impact the remainder of the diligence process. How quickly would deals move through the funnel, what new checks and balances were required to arrive at an outcome, and how could founders effectively build momentum to help investors develop confidence during the fundraising process?

How have you built confidence, without having met teams in person?

VCs have sourced from known founders and trusted networks to curb risk

In the early phases of COVID-19, some venture capitalists looked to de-risk investments by sourcing from founders known pre-pandemic, rather than building net new relationships. For Taylor Greene at Collaborative Fund, “50% of the entrepreneurs we invested in during this period were people already known before the pandemic.” This approach was echoed by investors at Underscore VC, Bloomberg Beta, Lerer Hippeau, and Upfront Ventures.

While always core to diligence, social validation behind a business and management team became even more critical determinants of fit. Investors looked to known, credible networks, to closed communities, and sought warm introductions to source new deals. Familiar loops offered invaluable, pre-seeded confidence.

Lily at Underscore VC commented that “while sourcing from trusted people has always been important to early stage investing, it felt particularly critical during this period of time. We looked to who from our respected community could help us meet founders, partnered closely with co-investors we’d worked with before and with credible angels.”

Hearing this feedback, we questioned potential implications for first-time entrepreneurs. In a world where a focus on founder track record and network became increasingly pervasive, how could new founders effectively break in and obtain early financing?

On opportunities for new entrepreneurs, James Cham from Bloomberg Beta opined: “Warm introductions and social context matter more than ever. Join online networks, reach out to investors over Twitter, and expand your community.”

Communication with management teams has become higher touchpoint, shorter form, and more transactional

The pandemic has perpetuated a range of more short-form communication styles between investors and entrepreneurs.

Rebecca Kaden at Union Square Ventures commented on this trend: “We lost the chatter from onsite visits, but we wound up having much more frequent and targeted touch points throughout the lifecycle of a deal, often through text, Signal, and WhatsApp. Rather than wait for an in-person exchange, if you thought of a question, you looked to answer it now.”

These same facilitating systems have also made the process feel more transactional to some. For Greg Bettinelli at Upfront Ventures: “as a relationship-driven investor, I feel like I’ve lost a degree of the interpersonal. There is less getting to know each other and more talking deals.”

Rebecca added “I think these new mediums accentuate the value of good storytelling. As both a founder and an investor, you need to be able to capture and keep interest pretty quickly.”

VCs are conducting more diligence and employing more founder references

Investors are now having more one-on-one conversations with founders over Zoom than they would have in person, even finding opportunities for more casual formats–the new ‘virtual happy hour’–to cultivate personal connections. 5 out of the 8 investors we spoke to reported that diligence had deepened during this period, relative to before the pandemic.

Taylor Greene at collaborative commented: “I’ve found that vetting a founder takes more reference calls, more Zoom calls, more ‘getting to know you’ calls. It has always been, but is increasingly a multi-step process.”

By all accounts, there is a degree of nuance lost without in-person communication, but reference calls and credible external perspectives have helped fill in the gaps–rounding out and even adding additional color to a person, team, and market.

One firm reinforced the growing importance of founder references during diligence: “We’ve invested more hours in diligence than alternatively. There is no doubt, particularly with early stage, energy, tenacity, and drive are important determinants of people. You lose that online. So, we have to rely more on other people to make up for that lost signal.”

Some venture capitalists have also looked inwards to collect perspective, involving more investors across their firms in deal evaluation.

Graham Brown at Lerer Hippeau commented on the move to include more investors in the decision making process: “Before COVID-19, 2 people had to meet the team before making a decision. Now, we’re trying to get more perspectives on an individual or a team by having 3 or 4 of us meet them. Ultimately, I think we’re moving to a culture that is more conviction based, but consensus driven–where everyone has a perspective on the team from having spent time with them.”

What impact do you think that this period will have on the quality of investment decisions?

While the real effect of COVID-19 on the quality of VC decision making remains to be seen, we heard varying perspectives on if impacts would be positive or negative. Here are the positives:

Virtual decision making may remove bias from the decision process, leading to better, more data-driven outcomes

When meeting a founder in person, aspects of charisma and likeability can yield an outsized impact. Some commented on the potentially harmful role of implicit bias: “I would argue that there may be some false positives that come when you get a great, charismatic person in the room, and that this can skew decision making.”

The idea that CEOs must have charisma can lead investors to overlook promising candidates, and to consider others unsuited for the role. Said Graham from Lerer Hippeau: “Not every founder has to fit the archetype of overtly charismatic to be a good founder, and rather many of the best founders do not. We tend to overweight star power when evaluating in person.”

In fact, while a study presented in HICSS confirms that hubristic and charismatic entrepreneurs have historically been more successful in sourcing capital, research from Harvard Business Review suggests that excessive charisma over humility can ultimately destabilize organizations in dangerous ways. Recent history has paved a growing cautionary tale around rapidly capitalized, excessively charismatic founders. Elizabeth Holmes of Theranos saw a once $9 billion valuation dissolve into 12 felony fraud charges. WeWork, steered by a particularly emphatic Adam Neumann, fell from a nearly $50 billion valuation to just $2.9 billion in under a year.

Perhaps, the most positive outcome of moving online is that we become less captivated by showmanship, more discerning, and more reliant on impartial references and predictive data. Kent Bennett at Bessemer Venture Partners offered: “Subconsciously, the element of bias towards charisma has flowed away and become less important on Zoom. I wonder, should it have ever been important?”

James at Bloomberg Beta offered an alternative view, that as founders and VC adapt to virtual modalities, charisma increasingly translates over Zoom. He added: “As usual, people adapt and become more comfortable online.The question remains–will different people succeed and translate better over Zoom than others? Who will be the charismatic person in this environment?”

More diligence, checks, and infused perspectives may ultimately lead to improved results

As investors funnel even more time into deepening diligence and building external context around management teams, the decision evaluation becomes more grounded in data and input collection versus blunt intuition. Lily Lyman at Underscore VC commented, “my hunch is that decisions will be better, because we’re forced to be more discerning. It’s forcing VCs to do more proactive work versus intuition work.”

Historically, ‘intuition’ has been a significant driver of early stage venture capital investments. A 2019 Pitchbook Survey administered to 391 VC investors, found that while only 38% of VC investors currently used data to source and evaluate all investment opportunities, 85% of respondents believed that investment decisions would always involve intuition. While some degree of intuition may always play into decision making, there is a growing appetite for data: 86% of survey respondents agreed that data is increasingly important to accurately assessing opportunities.

As Zoom-constrained venture capitalists push for more diversified inputs about a team and concept, more intentionality and fact-based evaluation may yield positive performance impact. One firm commented “Early sourcing and early diligence has been better and more data-driven than it’s ever been. I think we’re going to be able to end up as a more efficient and strategic group as a result of this.”

And here are the negatives:

Increased risk aversion may add more funding hurdles for underrepresented founders

The heightened atmosphere of caution surrounding the pandemic has introduced additional funding barriers for underrepresented and diversity founders. Lily Lyman from Underscore VC spoke to this directly: “When investing in known founders feels like the least risky path, how do we make sure that we expand diversity in our founders? This is an important question we’re doing the work to answer at Underscore.”

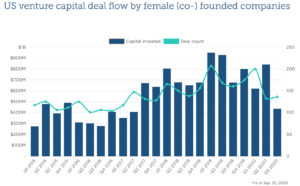

Recent data adds weight to these concerns. An October 2020 Pitchbook study reveals that venture funding for female founders has now hit its lowest quarterly total in 3 years. Firms invested $434 Million in female founded companies in Q3, the lowest since Q2 2017. This third quarter total also amounts to a 48% drop in funding from Q2.

This is a serious step in the wrong direction, and it has never been more critical to be cognizant of and intentional in reducing bias and enabling opportunity.

At NextView, we’ve taken proactive steps to dispel bias and increase our purview beyond our own known networks. David Beisel, co-founder and partner at NextView commented: “one of the motivations for our launching a virtual accelerator during the pandemic was to push ourselves to make sure we saw founders outside of our normal networks. We knew that the bias during this period would be to skew towards known founders and trusted referrals. But some of the best founders are off the beaten path, and we wanted to provide an avenue for that”

Gained efficiency may not necessarily correlate with better decision making

While most tout cutting out travel and gained efficiencies as positive outputs of this period, some cautioned that speed, and the increased ease of writing a check, may ultimately impair quality of decisions.

Rebecca Kaden from Union Square Ventures commented: “Part of writing a check meant getting to where the company was, coordinating logistics, and following steps that served to slow down the process. There were built-in roadblocks to moving too quickly.”

On the direct impact on decision making, she added: “There is nothing structural to slow investors down now and it’s becoming easier and easier to write a check. If you look at history, speed of decision making and investing generally haven’t correlated well.”

We may miss out on predictive nuance and meaningful, long-term relationships

Despite an inundation of new Zoom features (cue branded ‘virtual backgrounds’), subtleties still get lost online. It is easier for investors to get distracted by the growing backlog of emails, succumbing to the urge to multi-task rather than dedicating full attention. This may ultimately mean missed signals in the early phases of diligence.

Kent Bennett at Bessemer Venture Partners spoke to the importance of noticing subtleties: “You can sniff out when someone is being honest or dishonest in person, much better than you can on Zoom. Every signal from how they interact with other people in the office to how they conduct themselves in a boardroom may ultimately be core to the investment decision.”

Additionally, some venture capitalists have cautioned that this period may impede the formation of long-term relationships between VCs and their portfolio companies.

For Greg Bettinelli at Upfront Ventures: “Tactically, you can have a call, but it’s more challenging to build rapport over Zoom, to cultivate mutual trust as the foundation for a long-term connection. It’s not just about my getting to know the founder. If we’re going to partner together, I want them to vet and connect with me, and that’s harder to do in both directions right now.”

James at Bloomberg Beta offered a slightly different take: “Yes, l agree that we might have a deeper relationship with the person face to face, but I’m not sure I’d make a better decision or see a better outcome.”

What will be the long-term implications of the proliferation of virtual decision making?

Regardless of observed returns, the broader macro market may make it near impossible to discern the real correlation between remote decision making and outcomes. Rebecca Kaden commented: “If decisions are not as good during this COVID period, it may be hard to tell whether that’s due to changes to decision making from how the pandemic has changed our processes, or the general speed/heat of the current venture market.”

All 8 of the interviewed investors agreed that, while there will always be space in in-person interactions, elements of virtual communication are here to stay. Even as the dust settles on this period of crisis, there will be less flights taken for repeated cross-country board trips, more flexibility with staff location, and a renewed appreciation of the business value in remote work, both within firms and across portfolio companies. Many founder introduction calls will still happen virtually, to maximize efficiency and widen the top of the deal funnel.

However, showing up in person will remain core to the fundraising process, enabling investors to deepen relationships with founders and gain a competitive edge in the deal process. Rob Go from NextView offered his take: “Showing up in person will still matter significantly, especially if you are trying to win a deal and build rapport. In the end, the ability to meet in person may end up being how you stand out. If more VC’s go entirely remote, it could ultimately create more of an advantage for those who are willing to get on planes.”

As a large volume of VC firms concurrently raise new funds, firm differentiation is becoming even more critical. Through the third quarter alone, US VC firms have already raised $56.6 billion across 228 funds, with 2020 tracking to set a record high for total capital raised. Faced with growing deal competition from other firms, investors will need to proactively seek opportunity to gain advantage. In-person may be that edge. Rob prompted: “In the future, who will be willing to show up and go the extra mile?”

For now, we’ve been taking steps where we can — adjusting to meeting teams through screens and even embracing social distanced walks with founders, when feasible. We have connected with some truly inspiring teams throughout this period. Their stories resonate, both in person and virtually. We look forward to continuing to hear them.