HBS Entrepreneurs Founded the Most Startup Unicorns of Any MBA Program

As a second-year Harvard Business School student and NextView Ventures MBA Associate, constantly keeping up-to-date with the start-up world, I have heard some skepticism about the ability of MBAs to found top companies. Perhaps most famously, Guy Kawasaki quipped that the value of an MBA to an entrepreneur is “probably about a negative $250,000.”

There has been some fantastic recent work around debunking this common misconception, including Dimitri Dadiomov’s “Should We Take Harvard MBAs Seriously as Startup Founders,” Flybridge General Partner and HBS Professor Jeff Bussgang’s “Unicorns and MBAs,” Poets and Quants’ “Top 100 MBA Startups,” and PitchBook’s “The Top Universities Producing VC-Backed Entrepreneurs.”

As of January 20, 2016, based on the “CrunchBase Unicorn Leaderboard,” there are 157 unicorns (companies with $1 billion+ valuations) which have not IPOed or been acquired—and more start-ups reaching unicorn status every day. Unicorns have been over-hyped during the past few years, and nowadays frequently attacked by skeptics. Though, this article is not a reflection on the fundamentals of unicorns—rather, I am using them as a proxy for situations in which founders have executed on big ideas.

The question is, can MBA entrepreneurs really think big?

Key Insights

- 38 unicorns, or 1 in 4 (24%), have at least one MBA founder

- 63 MBA founders are represented among the 157 unicorns

- MBA unicorns are valued at $65 billion (of the total $533 billion unicorn valuations) and have raised $15 billion in funding (of the total $82 billion unicorn funding)

- Entrepreneurs from Harvard Business School founded the most unicorns (13), with Stanford GSB (7), Wharton (5), and INSEAD (4) rounding out the top four. (Editor’s note: We acknowledge that HBS has larger class sizes, a factor to consider throughout this report.)

For more detail and context, let’s dive into the analysis.

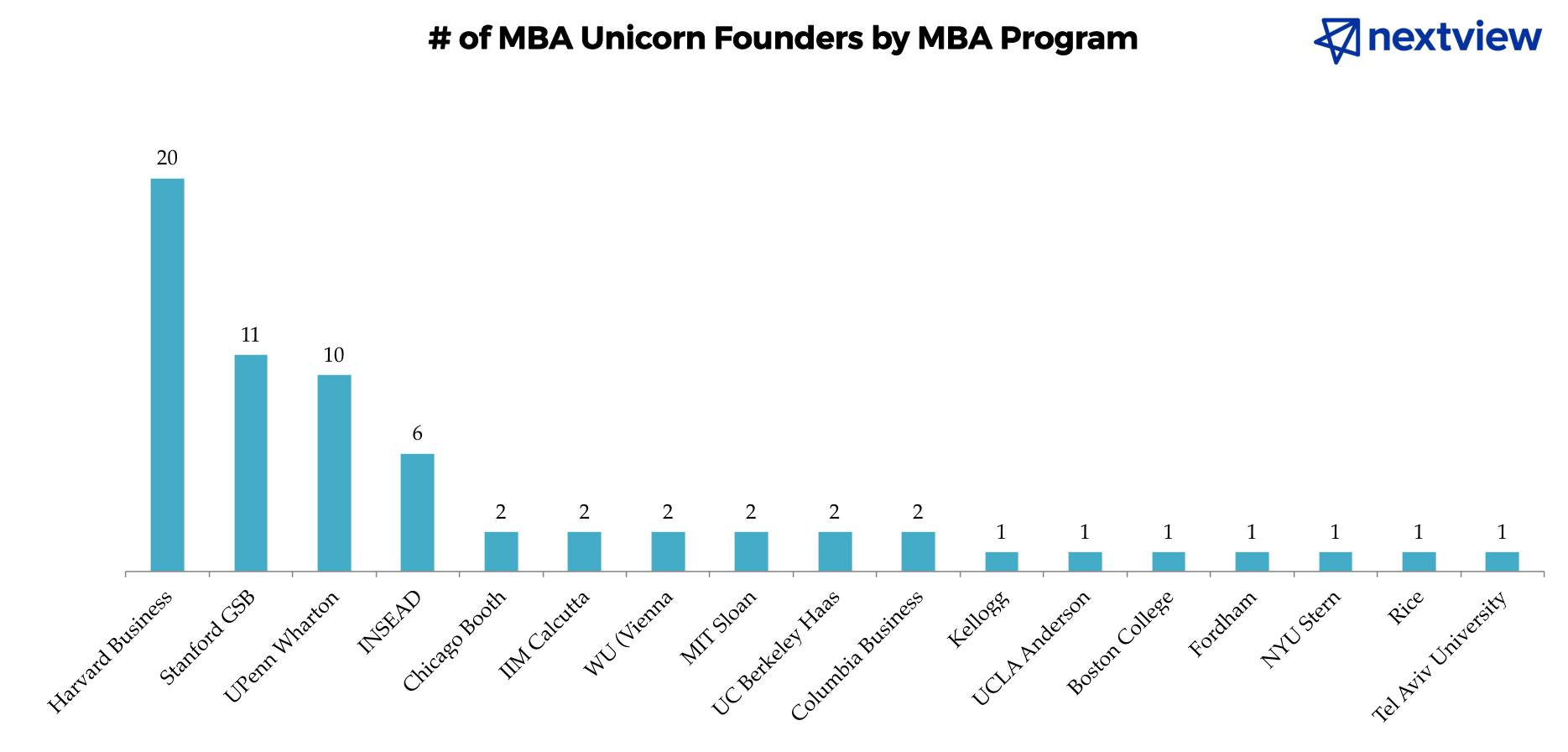

Harvard Business School and Stanford GSB Have Generated the Most MBA Unicorn Founders

MBA-Founded Startup Unicorns – NextView MBA-Founded Startup Unicorns – NextView

As you can see in the above graph, 18 MBA programs are represented among the 157 unicorns. As a Stanford alum and current HBS student, I was happy to see the MBA programs of both schools at the top of the list. Another interesting data point is that the top eight MBA programs in the U.S. (as ranked by U.S. News)—Stanford GSB, Harvard Business School, UPenn Wharton, Chicago Booth, MIT Sloan, Kellogg, UC Berkeley Haas, and Columbia Business School—and eight of the top ten global MBA programs, are all on the list of unicorns.

Five international MBA programs also boast Unicorn founders, namely INSEAD (France / Singapore / UAE), IIM Calcutta (India), Vienna University (Austria), Tel Aviv University (Israel), and University of Otago (New Zealand) (Please note that I only included MBA programs, and excluded Masters in Science degrees).

Of these MBA unicorns, 63 founders are represented. In fact, four of the unicorns were co-founded by entrepreneurs who hailed from multiple MBA programs:

- Global Fashion Group (HBS, INSEAD, Wharton, Booth, IIM Calcutta)

- Lazada Group (HBS, Kellogg, Sloan, Vienna University)

- Red Ventures (HBS, Wharton)

- Shazam (GSB, Haas)

Moreover, there are 12 MBA unicorns with multiple co-founders from the same MBA program. This data point indicates the importance of the business school network when founding a company, while also challenging the generalization that two or more MBA co-founders presents too much of a skill-set overlap.

- Global Fashion Group (3x HBS, 2x Wharton)

- ZocDoc (2x Columbia Business School)

- Oscar (2x HBS)

- GrabTaxi (2x HBS)

- Red Ventures (2x Wharton)

- Medallia (2x GSB)

- BlaBlaCar (2x INSEAD)

- Warby Parker (2x Wharton)

- Proteus Digital Health (2x GSB)

- ShopClues (2x WashU St. Louis)

- Cloudflare (2x HBS)

- Shazam (2x Haas)

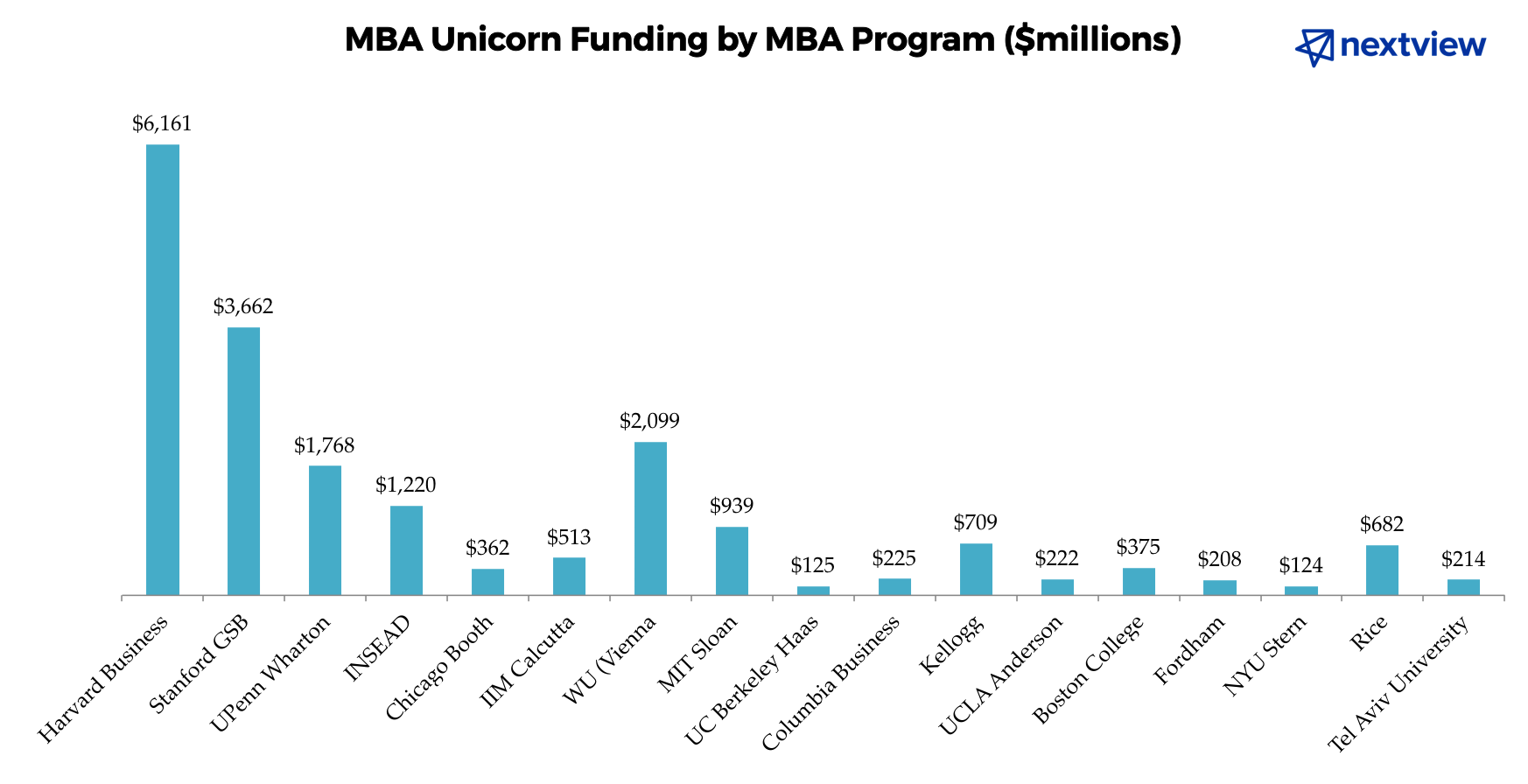

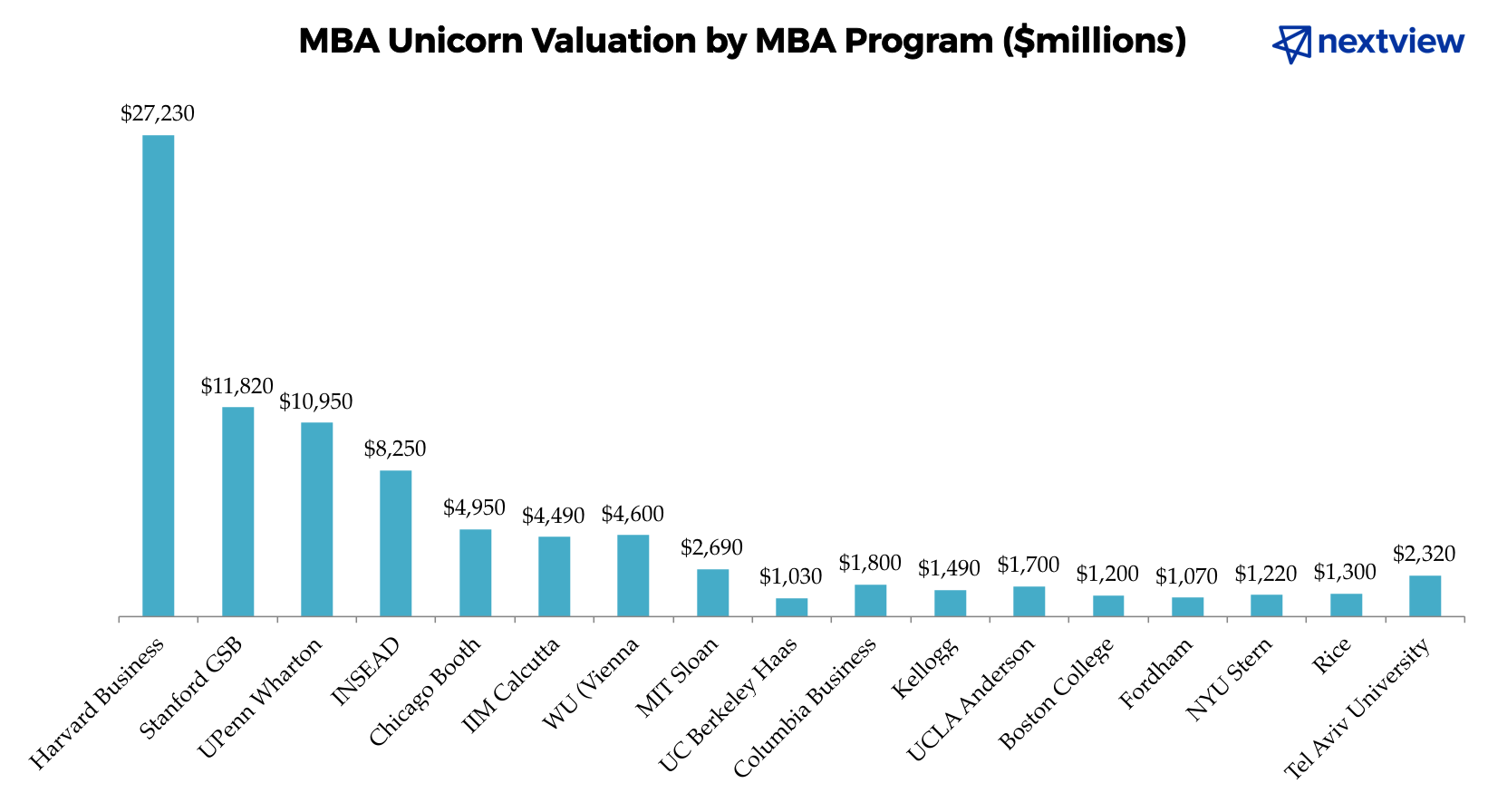

The above graphs illustrate that unicorns from Harvard Business School are valued at approximately 2.4x that of any other MBA program. Interestingly, though, it appears that Stanford GSB unicorns tend to raise proportionately more money, as the amount of funding received by Stanford GSB-founded unicorns over-indexes in comparison to HBS and Wharton valuations (HBS unicorn total funding is only 1.9x that of GSB). This is likely the case because of Stanford’s positioning in the Bay Area and the access to venture capital that accompanies it.

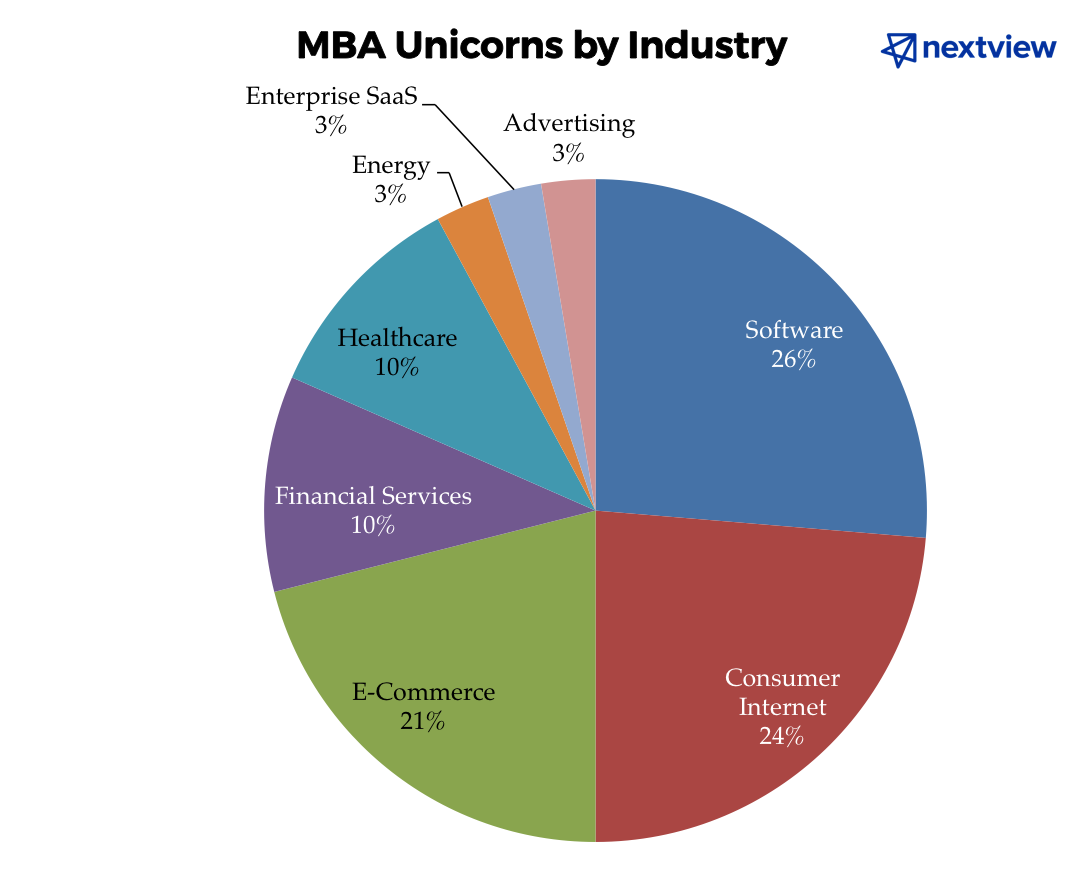

MBA Unicorns Weigh Heavily Toward Software, Consumer Internet, and E-Commerce

Unsurprisingly, software, consumer internet, and e-commerce companies make up the significant majority of MBA unicorns. Top MBA-founded unicorns in these three buckets are:

- Software: InMobi (HBS), Mu Sigma (Chicago Booth), MongoDB (INSEAD), and Red Ventures (HBS, Wharton)

- Consumer Internet: Dianping (Wharton), Delivery Hero (Vienna), Houzz (Tel Aviv), and GrabTaxi (HBS)

- E-Commerce: Coupang (HBS), Global Fashion Group (HBS, INSEAD, Wharton, Booth, IIM Calcutta), Blue Apron (HBS), and Honest Co. (UCLA Anderson)

When comparing MBA-founded unicorns to the entire set of 157 unicorns (above), you will see a similar proportion of software, consumer internet, and e-commerce unicorns (69% overall, vs. 71% for MBAs). However, as indicated by the sections of the pie with thick black outlines, industries such as hardware, security, and aerospace & defense are represented in the overall set of unicorns, but not in the MBA-founded selection. My hypothesis is that there are two forces at work to explain these data points:

- Overall, in the past few years, investors have been more eager to invest in asset-light companies, so fewer capital-intensive start-ups (such as those in the energy, hardware, aerospace, etc.) have reached unicorn status.

- MBA founders without strong engineering backgrounds are more likely to found companies that require less technical expertise.

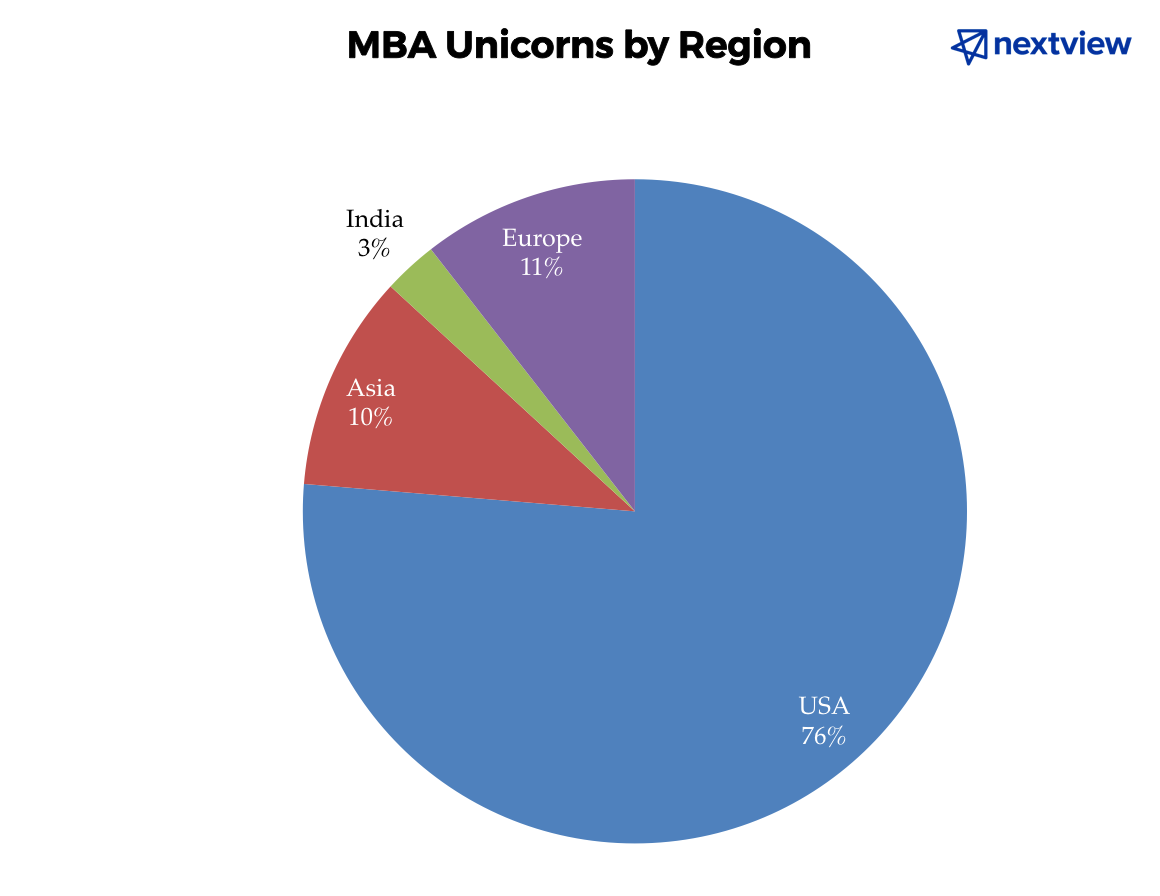

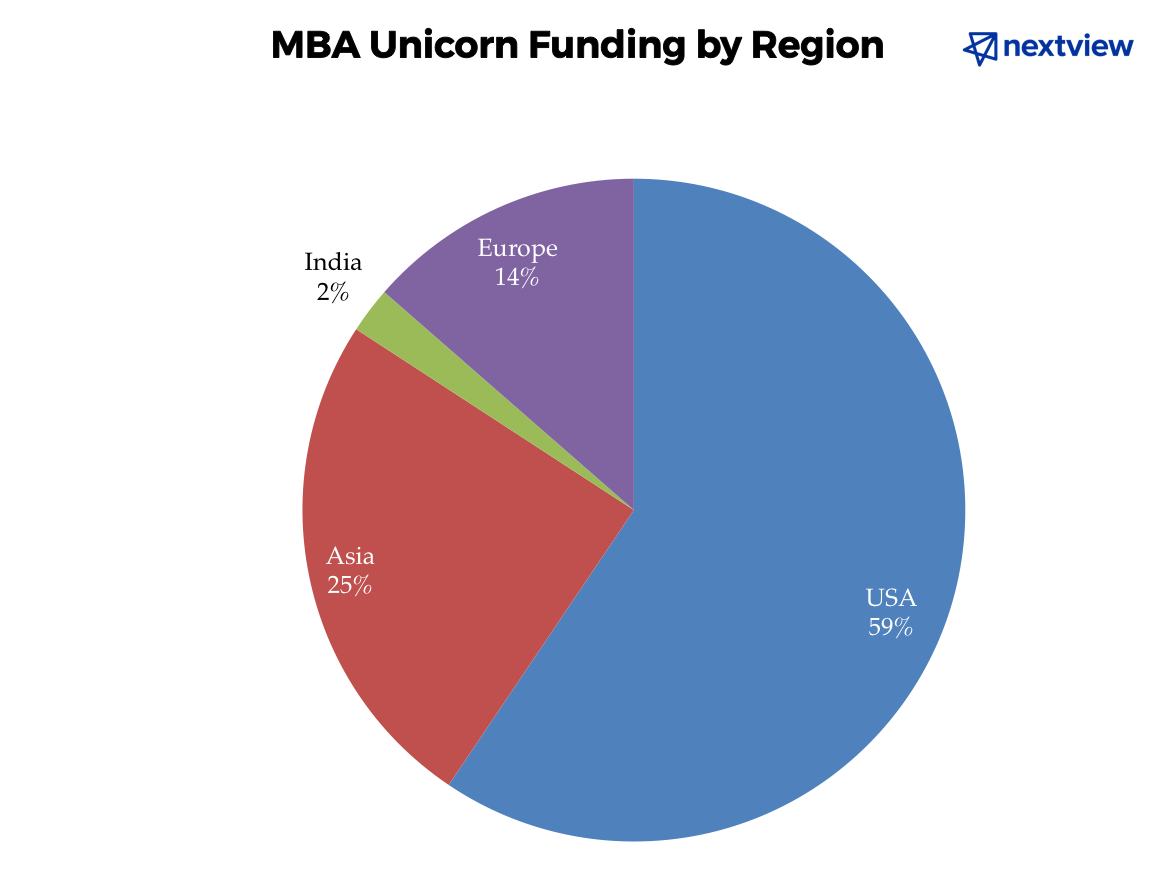

Most MBA Unicorns are Headquartered in the U.S.

Finally, as the above charts illustrate, three-quarters of MBA unicorns are based in the United States. Interestingly, MBA-founded unicorns in Asia, India, and Europe appear to command proportionally higher valuations and funding than those in the U.S.

Below are the top MBA-founded unicorns headquartered in each region:

- USA: SoFi (Stanford GSB), Moderna Therapeutics (HBS), Houzz (Tel Aviv University), Blue Apron (HBS)

- Europe: Global Fashion Group (HBS, INSEAD, Wharton, Booth, IIM Calcutta), Delivery Hero (Vienna University), BlaBlaCar (INSEAD), Funding Circle (Stanford GSB)

- Asia: Coupang (HBS), Dianping (Wharton), GrabTaxi (HBS), Lazada Group (HBS, Kellogg, Sloan, Vienna University)

- India: ShopClues (Washington University St. Louis), Quikr (IIM Calcutta)

As you can see in the above graphs of all 157 unicorns, MBA founders over-index on unicorns headquartered in the United States (74% vs. 63%). This U.S. focus is likely due to the fact that only five international MBA institutions graduated Unicorn entrepreneurs, accounting for 11 of the 63 total MBA founders. In fact, 7 of the 11 MBA founders from international programs founded five of the ten MBA unicorns headquartered outside of the U.S.:

- Global Fashion Group (Luxembourg): INSEAD, IIM Calcutta

- Delivery Hero (Germany): Vienna University

- Lazada Group (Malaysia): Vienna University

- BlaBlaCar (France): INSEAD

- Quikr (India): IIM Calcutta

Conclusion

When I initially started this research, I hoped that the percentage of unicorns founded by MBAs would be higher—perhaps closer to 50%. Finding that the reality was only half of that, I was a little bit disappointed at first. However, once I thought about it more in-depth, putting it into perspective, I realized how impressive the one-in-four statistic really is:

- On average, the top 10 U.S. undergraduate universities graduate three times the number of students each year than the top 10 U.S. business schools.

- There exist many more undergraduate institutions around the world than business schools—with large public universities skewing the numbers even more.

- There are thousands of other graduate programs which produce eventual start-up founders.

- Not to mention, there are tens of millions of adults in the U.S., and billions of adults in the world, without college degrees, who have the potential to found top companies.

Finding that the comparatively tiny group of MBAs founded 25% of the top start-ups is actually pretty remarkable in context. The statistics bring up a number of important points for MBAs and investors to consider:

For those looking to start companies, business school is an excellent place to develop skills, learn from some of the brightest people in the world (both professors and classmates), think introspectively, and build out a strong network. It is also a unique opportunity to contemplate start-up ideas with professors who are top thought leaders in their fields, leverage b-school resources to incubate ideas, and find co-founders. Not to mention, these skills and connections are extremely valuable in the long-run for building sustainable businesses and raising money from investors—if the entrepreneurial spirit happens to kick in years after graduation. Take full advantage of your MBA when founding a company, rather than thinking that it devalues your venture in any way.

Also, I hope to see future MBA entrepreneurs working to solve big problems outside of the U.S. and in more technical areas, such as hardware and energy. This may come to fruition as business schools accept more STEM students, and venture capital investment in Asia and Europe continues to grow.

For venture capital investors, these findings indicate that VCs should focus more than they do on the top business schools to source potential high-flying investments. Investors should particularly keep an eye on start-ups from MBA programs such as HBS, Stanford GSB, Wharton, and INSEAD. It is not just the Computer Science Master and PhD students starting the most exciting companies…

Overall, this exercise convinced me that MBA founders are not only useful for helping to scale mid-stage-plus start-ups—they also have a high potential to envision and execute on big, visionary ideas. I look forward to seeing (and hopefully investing in) the amazing concepts that my classmates bring to fruition in the near future.

Please see the following Google Spreadsheet for the raw data used in this analysis, and feel free to reach out to me at dkf@nextviewventures.com with any questions and/or comments.