Airbnb S-1 (Part 1): So How Profitable Is This Thing Really?

Airbnb’s public S-1 dropped Monday afternoon. One of the most highly anticipated startup IPOs of recent years, we now get a peek inside Airbnb’s business.

You can read various articles out there which will give you the cursory facts about Airbnb like their overall revenue or profitability or how their business has faired here in 2020 in the COVID environment. What my part 1 analysis here seeks to cover (similar to my prior write-ups of the IPOs of Facebook, Alibaba, Slack, Lyft, Square, and more) is less obvious insights about Airbnb as well as as assessment of how attractive their long-run business prospects might be. I’m going to try to do a follow-up part 2 later this week specifically delving into Airbnb’s partial (though not complete) rebound here in the second half of 2020 in the midst of the COVID pandemic.

Let me start with the obvious… Airbnb is a remarkable company which is redefining the hospitality industry in a number of ways. Everybody has known that for awhile, even without perusing a prospectus. Since inception this lodging marketplace (note 1) has enabled 825 million guest stays in over 200 countries with a cumulative booking value of more than $110 billion. Along the way “Airbnb” has gone from brand name to a common noun in the same vein as using a “Kleenex” or drinking a “Coke”. Regardless of how the IPO unfolds or how Airbnb performs as a company in the coming years, the founders, team, and VC investors can rightly be proud of what’s already been accomplished over the last 13 years.

Source: Airbnb S-1

Airbnb’s Secret Sauce

There are two key things which have made Airbnb a killer business… the first, which generally gets all the attention, is the unlocking of a vast supply of new lodging inventory (see note 1). Private apartments and homes largely were not available for short-term rental prior to Airbnb, whereas now many are available for booking on a full or fractional basis. Airbnb’s availability as a marketplace and its aggregation of substantial consumer demand has actually meant certain forms of lodging have been newly built or converted into rooms for the primary purpose of listing on Airbnb. Airbnb has blurred the lines between what’s a “hotel” room and a private residence, which has at times caused conflict with local laws and regulations though they’ve largely been able to navigate these in a less adversarial way than other innovative marketplaces (e.g. Uber).

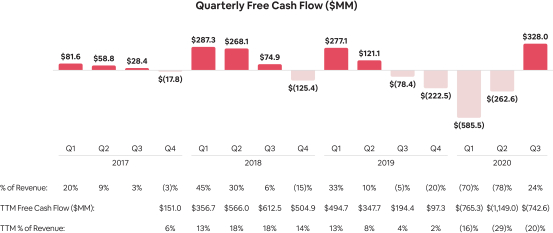

But the second ingredient in Airbnb’s secret sauce is at times overlooked… they flipped the traditional cash collection model of hotels and vacation rentals upside down. Hotels generally don’t require any cash up front for a booking and vacation rentals typically require a partial deposit but not the full booking. Airbnb convinced travelers to part with 100% of their booking cost up front and then they pay out the required amount to hosts when the stay actually occurs. Additionally Airbnb charges both sides of the booking (guest & host) a separate service fee. If you book a hotel through an online platform like Expedia or Priceline, as the traveler you pay nothing (OTAs charge hotels a fee).

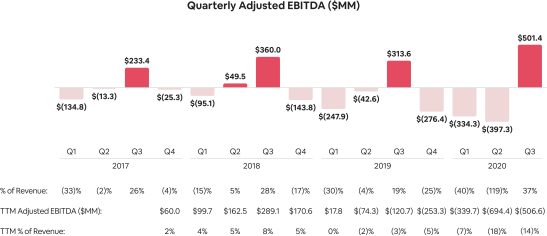

Airbnb therefore generates substantially higher free cash flow (FCF) than accounting profit. This is true not only in terms of GAAP net profit (most conservative representation of profit), but also Airbnb’s FCF is well above even its adjusted EBITDA (most liberal representation of profit, sometimes referred to in jest as “profit before the bad stuff”).

So How Profitable Could Airbnb Really Be?

I won’t bury the lead here… having spent hours digging through the S-1, I’m a little underwhelmed at how profitable Airbnb really is at present. Of course this begs the question of “compared to what?” so I’ve tried to do some very high-level comparisons of Airbnb to online booking platforms (aka OTAs) like Booking Holdings (Priceline, KAYAK, etc) and Expedia Group (Expedia, Hotels.com, HomeAway, etc) as well as hotel companies like Marriott and Hilton.

To be clear Airbnb posted a GAAP profit in Q3 2020 of over $200M which is impressive given travel remains materially depressed due to COVID. Airbnb’s bookings have rebounded to roughly 70-80% of what they were in 2019 pre-COVID whereas global hotel companies like Marriott and Hilton are operating at roughly 35-40% of where they were in fall 2019. But even with this profitable Q3, on a trailing twelve months (TTM) basis Airbnb has a GAAP net loss of >$1 billion.

Airbnb has a marked seasonality pattern to their profits and cashflows. Their FCF swells in Q1 and Q2 as new bookings peak and travelers pay up front as discussed above. From an accounting standpoint though Airbnb recognizes the actual profit when the stay happens, so Q2 has been close to breakeven and then Q3 shows a significant profit. This coincides with summer leisure travel, as many of us take vacations and more weekend trips in June, July, and August which straddle the end of Q2 and make up the bulk of Q3. You can visually see this pattern very clearly in the FCF and adjusted EBITDA charts above.

But wholly separate from any seasonal patterns, which disappear when you look at full year financials anyway, Airbnb spends a substantial amount running the business. The straight cost of revenue line is only ~25% of revenue implying a 75% gross margin, assuming you were looking at this in a simplistic revenue / COGS / gross profit manner. But ops & customer support is another 17-20% of revenue and arguably you couldn’t run the business if you took that away. Sales and marketing has been 30%+ basically forever, though undoubtedly Airbnb has enough brand recognition and loyal customers that if you turned off marketing spend then revenue would drop but not to zero. So even before you get to product development (20% of revenue) or G&A (14% in 2019), you’re already looking at a narrower potential margin than you might expect from a marketplace or transaction platform.

How does this all stack up against OTAs or hotel companies? Again looking at 2019 to make a pre-COVID assessment about any of these businesses and looking specifically at operating income (aka pretax) margins:

- Airbnb -10%

- Expedia 8%

- Booking Holdings 35%

- Hilton 17%

- Marriott 9%

Of course these other companies are more mature, more slowly growing businesses which you’d expect would have higher operating profits. Marriott & Hilton are slow single digit YoY growers and even the OTAs which are faster growing only have revenue CAGRs in the 11-12% range. Airbnb is still growing rapidly (revenue CAGR >40% thru 2019) and thus you’d expect they’d be investing more heavily in product development and marketing to continue fueling future growth, at the expense of near term profitability. For reference, high-flying megacap tech stocks like Apple and Google have operating income margins >20% and Facebook and Microsoft have operating income margins >30%.

So the big question is of course over the long run, both post-COVID and as a more mature business, what sort of profitability profile might Airbnb have? The bull case is that over time, Airbnb can reduce the amount they’ve been investing in both product development and sales and marketing thereby substantially increasing their operating profit margin. Airbnb has pretty strong revenue retention… their cohort data shows them getting 35-45% of first year revenue in years 2, 3, 4, and 5. Also it’s pretty obvious if you talk with someone in their 20s or early 30s… the brand affinity for Airbnb is strong, especially among younger travelers. So even as these generations progress in age it’s reasonable to think that Airbnb will continue to capture a larger share of lodging wallet relative to traditional hotels or other options.

The bear case for Airbnb’s long run operating profit margin is that travel is a category where you’re competing for a consumer’s business each time they book a trip. The whole reason the OTA category exists is because consumers want to shop various options for flights, lodging, etc based on price, availability, brand, etc. If this proves true, Airbnb can continue to gain share from traditional hotels but still have to spend fairly heavily on sales & marketing such that they have slimmer operating profit margins.

So Where Does Airbnb Go From Here?

For what it’s worth, I suspect that Airbnb will continue to grow fairly rapidly and continue to redefine the lodging category. They have many happy customers (myself included) and both the number of traveler customers and share of wallet from their most loyal customers is likely to grow. The company will undoubtedly go public with a significant market cap (estimates are pegging this in the $30B+ range) and it wouldn’t surprise me if the company performs well in the near term and ends up with a $40-50B market cap pretty quickly, particularly if expectations of COVID subsiding helps fuel a 2021 travel rebound. Make no mistake, I think Airbnb is a great company and will continue to be one for years to come.

But my analysis of the business, as described in the S-1 in great detail, leads me to believe that Airbnb will have solid but not exceptional profit margins in the long run. If that proves to be right, Airbnb may ultimately be a company where the majority of the value creation has occurred in the private markets over the last 13 years. Uber is an $85B+ market cap company today but is essentially flat to its IPO price and late private round valuations. Contrast that to companies like Square or Shopify, which have increased in value 20-50x since going public, and the overwhelming majority of value creation has occurred in the public markets.

======

Note 1: I refer to Airbnb as a lodging marketplace. While they offer “experiences” like guided tours and such, and lump all their revenue into a single “Nights & Experiences” bucket the reality is experiences is not a meaningful part of the business by Airbnb’s own admission (“Substantially all of the bookings on our platform to date have come from nights” – pg 119).

Fun Tidbit 1: Europe and North America are of similar importance in terms of revenue (40% EMEA / 41% N. America in 2019) though in terms of nights booked Europe was 43% and N. America was only 29% –> so per booking North America generates roughly 50% higher revenue than Europe